APRA’s needle just popped the housing bubble

/It is said that a bubble is just a bull market that you’re not in. A pithy one liner that neatly captures the fine line between good fundamentals and overvalued assets.

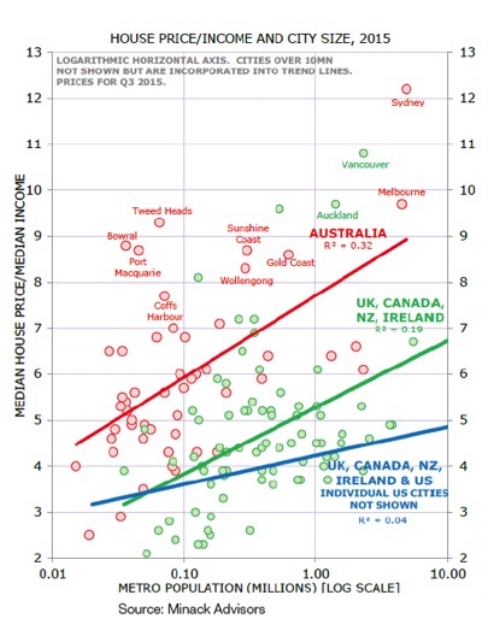

One way of looking at this housing bubble is to flip the question on its head: Given we have some of the most highly valued housing markets in the world (chart below), is the rest of the world just stupid? Is the sum of all the other views on housing misguided and we in Australia have found a new way of generating long-term sustainable wealth?

The most likely answer is no. The calamitous end to US housing stocks in 2007, has some similarities to now in Australia: regulatory bodies had become concerned and were raising interest rates; a very high portion of loans were on their version of interest only loans; and, importantly, supply had caught up and gone into oversupply. A lot of people claim now it was obvious it was a bubble, but large segments did not believe this to be the case.

It is within this context that the recent announcements by the Australian Prudential Regulatory Authority (APRA) are so important. In response to the increasing concerns about the Sydney (also Melbourne) housing market, a raft of measures to reduce the amount of bank lending was announced in early April. These included measures to limit further lending to investors beyond the previously announced “speed limit” of 10 per cent loan growth for investors; and to increase scrutiny of stated incomes and further stress tests on borrowers.

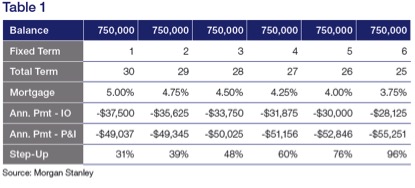

But the most important part relates to the new cap on Interest Only (IO) loans to 30 per cent of all loans (it is currently closer to 40 per cent on average). The reason why APRA’s move is potentially so important is that for investors who have multiple properties, the move to force repayment of principal will see their repayments balloon. Table 1 is a worked example of what moving to principal and interest does to the repayment schedule for a borrower with a loan book of $750k.

Given landlords are unlikely to put up rents by 30%-100%, particularly given the new supply coming online later this year. The more likely outcome suggests some investors become forced sellers later this year to reduce their outstanding loan book, adding to supply of properties that hit the market in 2017 and 2018.

Could 2017 be looked back as the “obvious” peak when supply collided with reduced borrowing capacity and overvalued assets?

Speak to Wynyard Park Private Wealth to discuss your property and investment options.