Are you prepared for the new superannuation changes?

/In November 2016, the Federal Government passed into law superannuation reforms that were first announced in the May 2016 Federal Budget. Importantly, these changes include reductions in the amount that can be contributed to superannuation, as outlined below:

■■ A lower pre-tax (concessional) contributions cap which includes the compulsory superannuation guarantee (SG) contributions made by your employer on your behalf as well as any salary sacrifice contributions you choose to make and, if self-employed, your personal deductible contributions.

■■ A lower after-tax (non-concessional) contributions cap which includes any after tax contributions you choose to make to super (including any capital gains you have made as a result of selling an investment property or receiving an inheritance).

What are the new caps?

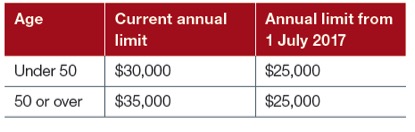

From 1 July 2017, new annual limits will apply to the level of contributions you can make to super, as outlined in the following tables:

Concessional contributions

Non-concessional contributions

Although the existing limits have been reduced, there are strategies that can help you ‘catch up’.

What are the ‘catch up’ strategies?

From 1 July 2018, if your super balance is under $500,000, and the concessional contributions you make each year are less than the allowable cap, you will be able to carry forward any unused portion to the next year, for up to five years.

For example, you make $10,000 in concessional contributions during the 2018/19 financial year and $15,000 in concessional contributions during the 2019/20 financial year. Over these two years, you have accumulated an unused portion of $25,000 that, once added to your annual concessional contribution cap for the 2020/21 financial year, allows you to make a higher concessional contribution of $50,000 in that financial year.

While not a new strategy, the new limits that apply to the amount of non-concessional contributions you can make also change the amount you can contribute under the bring-forward rules. If you are under age 65, you can bring forward three years’ of contribution limits to make a larger one-off contribution to your super. From 1 July 2017, these types of contributions will be capped at $300,000 and there are transitional rules that apply.

For example, if you receive an inheritance of $350,000 in the 2018/19 financial year, you could utilise the bring forward rules and make a $300,000 contribution to your super. In so doing, however, the next non-concessional contribution you could make would be in the 2021/22 financial year. Regardless of how close you are to retirement, strategies to maximise your superannuation can be used by everyone. Superannuation helps you to accumulate as much as you can towards your retirement nest egg while utilising the significant tax concessions that are available.

Speak to Wynyard Park Private Wealth to discuss your superannuation options.

Source: IOOF